Debt mutual funds invest in variously rated debt instruments ranging from sovereign rated to AAA to BBB to junk status and all those in between.

According to Investopedia “A debt fund is an investment pool, such as a mutual fund or exchange-traded fund, in which the core holdings comprise fixed income investments. A debt fund may invest in short-term or long-term bonds, securitized products, money market instruments or floating rate debt”.

As per SEBI’s categorization there are 16 different kinds of debt funds. These are:

- Overnight fund

- Liquid Fund

- Ultra short duration fund

- Low duration fund

- Short duration fund

- Gilt fund

- Money market fund

- Dynamic bond fund

- Corporate bond fund

- Medium duration fund

- Medium to long duration fund

- Long duration fund

- Credit risk fund

- Banking and PSU fund

- Gilt fund with 10 year constant duration, and

- Floater fund

How to analyse a debt fund fact sheet?

The monthly factsheet can be downloaded from the respective AMC’s website, mostly through their download section or by googling it.

For the purposes of this article, we’ll be looking at the factsheet of a corporate bond fund. This article is neither a review, nor a recommendation of the AMC/debt fund used as an example.

This section shows the name of the fund and its category along with a short note on the investment objective of the fund.

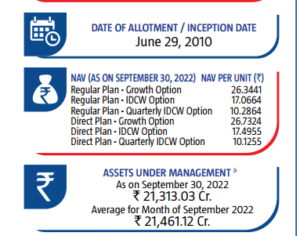

The section in the image above, shows the current NAV of the different fund options, the date of inception of the fund as well as the total assets under management of this fund.

This section, shown above, provides the fund portfolio details including:

- The name of the securities being invested in, their maturity date and their issuer

- The credit rating of the securities and the name of the credit rating agency used by the issuer

- The percentage of the respective securities’ holdings as a percentage of the total fund portfolio.

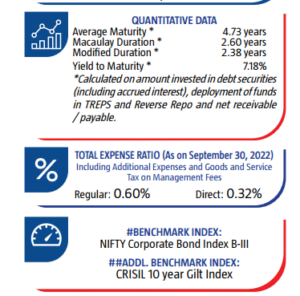

This section, shown above, provides data regarding the average maturity of the invested securities in the fund portfolio, and their modified duration.

An important piece of information given here is yield to maturity (YTM) which is defined by Investopedia as “the total return anticipated on a bond if the bond is held until it matures”.

This is important since the more the timeline of your goals and that of the invested securities are in alignment the better it is, keeping in mind the risks like interest rate risk and re-investment risk.

This section also provides the expense ratio of the fund, which is deducted from the fund’s NAV on a daily basis. The option to always go for is the “direct” option provided you have understood the credit default risk in the portfolio especially if it is a medium to longer duration debt fund. The respective index against which the fund is benchmarked is also shown at the bottom of the above image. Fund factsheet October ’22The image on the left shows the portfolio classification by credit rating of the securities.

The nearly 67% holding of the non-sovereign rated securities, shown in the classification section above, carries a degree of credit default risk.

Though the lower-rated securities potentially provide a higher YTM, they also carry a higher default risk in the form of loss of capital.

The image above lays out the past performance of the fund. However, a debt fund is impacted by interest rate movements. Any increase in interest rates lowers the bond prices and a decrease in interest rates would lead to an increase in bond prices. On the other hand, an increase in bond prices lowers bond yields and vice versa. As the last para on the above image says, past performance is unlikely to be sustained in the future.

A summary of the key points to look for in a debt fund factsheet:

- Higher the AUM, higher is the liquidity of the fund.

- Lower the rating of the securities invested in, higher is the risk of credit default.

- Is the maturity of the fund’s invested securities aligning with your timeline requirements for this investment?

- YTM of the portfolio and the risk trade-off. Can a fund with higher YTM having a high-risk portfolio be replaced with a fund with 50-100bps lower YTM but with far lower credit default risk?